A reader asks:

I hate my job. Can you help me retire in 10 years? I’m already 45 years old and have only about $1 million saved. I am the only income earner out of a family of four with a wife + 2 grade school children. I make about $300k+ a year. I plan to max all my tax advantage contributions every year totaling about $80,000 + another $50,000 into a taxable account. I spend an average of $12,000 total for the family per month including mortgage, car, expenses and vacations. How should I invest so that I can retire at 55? How much do I actually need to retire at 55 while supporting the family? I’m thinking $3.5 million but even that is worrisome. Also what growth rate do you assume year over year? I use 4% or 5%, which gives drastically different numbers. I do have about $30k in cash savings but plan to build that up to about 3 years of expenses. Did I mention I hate my job?

This is like the Voltron of financial planning questions.

Everything comes together — retirement planning, financial market return expectations, portfolio management, saving money, liquidity provisions and the intersection of your career with your investment plan.

I’m not sure what it is about round numbers that makes us feel more comfortable. No one ever dreams of retiring early at age 54 or 57. It’s always 55 or 60. But I digress…

Being a millionaire in your mid-40s is good work. Saving more than 40% of your pre-tax income is also commendable. I’m guessing the savings rate is so high because I’m pretty sure you hate your job.

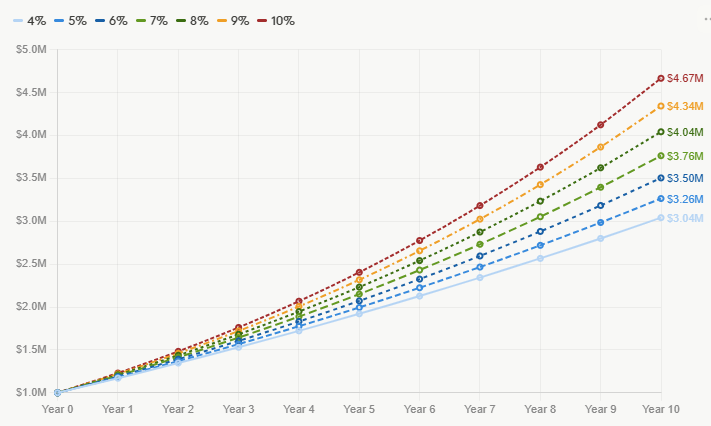

I’m guessing the $3.5 million goal came from the 4% rule. Spending $12k/month is $144k/year. If you divide $144k by 4%, you get $3.6 million.

Based on the assumptions given here — $1 million starting point plus $130k of annual savings — you’re right on track given a range of potential returns:

Financial freedom is in sight.

The only question is does it come at 55? Or 60? Maybe 65?

That depends.

Your money has to last longer when you retire early (duh).

Setting return expectations is never easy. No one can predict these things. Pundits have been predicting a new normal of lower stock market returns since 2010 yet we’ve continued to see double-digit annual returns for years on end.

Will it continue? I don’t know. I do like the fact that you’re being conservative. That builds a margin of safety into your plan.

I like the idea of building a cash reserve heading into retirement too. That cushion is important.

My only quibble here is the ratio of tax-deferred to taxable brokerage savings. A taxable account offers more flexibility in early retirement since those tax-deferred accounts have rules on when you can begin drawing them down.

There are other considerations that could throw a wrench into your plans.

You spend $12k/month today. In 10 years at a 3% inflation rate that’s more like $16k/month or $192k/year in spending. How negotiable is your lifestyle?

In 10 years, you’re also looking at potentially having two kids who are going to college. Are you paying for that?

What’s your plan for healthcare in early retirement?

I’m not trying to throw cold water on your plan here, but it is helpful to go through this exercise because it forces you to look at all the different variables involved in the retirement planning process.

You have three legitimate options here:

Option 1. Roll the dice and hope everything works out. Financial markets could keep on keepin on and give you an even higher balance than you’re currently planning on.

Maybe your kids will get a free ride to college or start their own AI business.

But what if that doesn’t happen?

Option 2. Get a new job that doesn’t make you so miserable.

Would you be willing to take a pay cut to increase your happiness and maybe work a little longer?

The stress and dread you get from working in a job you hate is going to compound even faster than your portfolio in the next decade.

Do you have other options?

Option 3. Hire a financial advisor.

All of the variables involved in the early retirement planning process can be overwhelming. A good financial advisor can help you understand how close you are to turning your dream into a reality.

You already have a goal in mind which is half the battle for many people. You can create your plan with a clear goal in mind, update it as time goes by, and have an independent third party offer guidance along the way.

A good advisor can also walk you through the trade-offs of retiring at 55, taking a lower salary, working longer, changing your spending habits or a whole host of other options.

This process is highly uncertain because of all the variables involved. Working with a planner can often uncover parts of the planning process you didn’t even consider.

I covered this question on an all-new episode of Ask the Compound:

Jonathan Novy joined us on the show this week to cover questions about life insurance, variable universal life insurance policies, how to get your adult kids to save money and how to spend down your college savings.

Further Reading:

The 4 Year Rule For Retirement Spending