A reader asks:

When I opened a Roth IRA in my early 20s, I went 60/40 because a 100% stock portfolio felt reckless, even though I had 40 years ahead of me. The Scottrade rep helping me at the time actually chuckled and tried to nudge me toward more stocks. I knew the math favored them too, but bonds just felt safer. What’s the argument that actually moves the needle for a young investor who intellectually gets it, and has even been told directly, but emotionally still can’t pull the trigger on a stock-heavy portfolio?

Another reader asks:

I have been managing my own portfolio for over 30 years. It contains mostly ETFs and a small carve-out of a stock portfolio for the love of the game. I have avoided having bonds in my portfolio my entire life. Any cash I raise occasionally has been kept in money market funds. I don’t have the comfort around bonds like I do with equities, but the other part is psychological as I am always thinking about opportunity costs. I am nearing retirement now and it’s time to step partially off this crack ride of equities and take some of my winnings and put them into bonds. I just really struggle with making the move to even a 10% bond portfolio and don’t know where to begin or how to get myself to stop thinking about the stock market gains I will be sacrificing.

We have a young investor in their 20s who is more conservative by nature and invested in a 60/40 portfolio.

We have an older investor, fast approaching retirement, who is more aggressive by nature and wants to invest 100% in stocks.

On paper, these investors are completely backward.

Your biggest assets as a young investor are time and human capital. When you have multiple decades ahead of you to save, invest and deploy your capital, you cannot invest aggressively enough.

Your biggest assets as a retiree are financial assets. You have more to lose. This is why most investors begin a glidepath toward more conservative investments with a portion of their portfolio in the lead-up to retirement.

On paper, the young person should be the one with 100% in stocks and the retiree should be the one with the 60/40 portfolio. This seems suboptimal and even irrational in some respects.

Here’s the thing — every investor is irrational in some ways. And that’s okay…as long as you understand the trade-offs being made.

You can have a balanced portfolio in your 20s if it helps you sleep at night but the opportunity cost is the wonderful long-term returns in the stock market.

You can have a 100% stock portfolio in retirement if that helps you sleep at night but you open yourself up to the possibility of big losses at inopportune times.

Since 1950 the S&P 500 has experienced:

- 39 drawdowns of -10% or worse.

- 11 drawdowns of -20% or worse.

- 3 drawdowns of -40% or worse.

This is why some investors need an emotional hedge. It can be a painful experience to witness your hard-earned life savings lose 40% of its value.

It’s also why it can be so difficult to hold an equity-only portfolio in retirement. You don’t have as much time or future savings to wait out a bear market. Selling stocks when they’re down can be a recipe for disaster if you happen to have a bear market early in your retirement years.

But some people understand these risks and keep all of their money in stocks anyway.

The truth is your asset allocation depends on many factors.

There are factors you can quantify such as your goals, expected returns and volatility characteristics. Some people are more inclined to manage their finances through spreadsheets.

But there are also qualitative aspects of investment planning that are more difficult to define like your personality, inherent biases and emotional disposition.

Investing is a form of regret minimization. Some people will regret taking part in big losses and bone-crushing volatility. Others will regret missing out on big gains and are content to sit through the pain and wait it out.

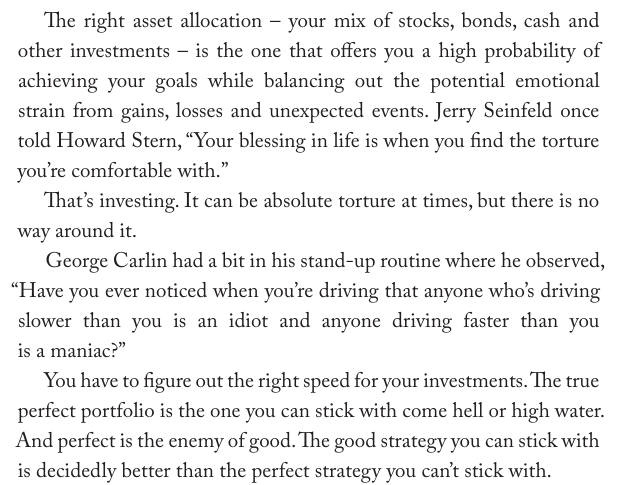

As long as you understand the trade-offs, there is no optimal portfolio. In fact, the sub-optimal portfolio you can hold onto is much better than the optimal portfolio you give up on. Giving up on your investment strategy is indistinguishable from a failed plan.

The last chapter of Risk & Reward is titled “The Perfect Portfolio.”

Here’s a passage from the book that sums up my thoughts on both of these questions:

You have to understand yourself when making financial decisions.

The numbers are important but so are the emotions.

If you can’t control your emotions it doesn’t matter what your portfolio looks like.

We covered both of these questions on an all new Ask the Compound:

We also covered questions about energy stocks, selling your soul for a job you hate, disagreeing with your spouse about portfolio management and when to raise some cash in your stock portfolio.

Further Reading:

Can You Live Off Your Dividends?