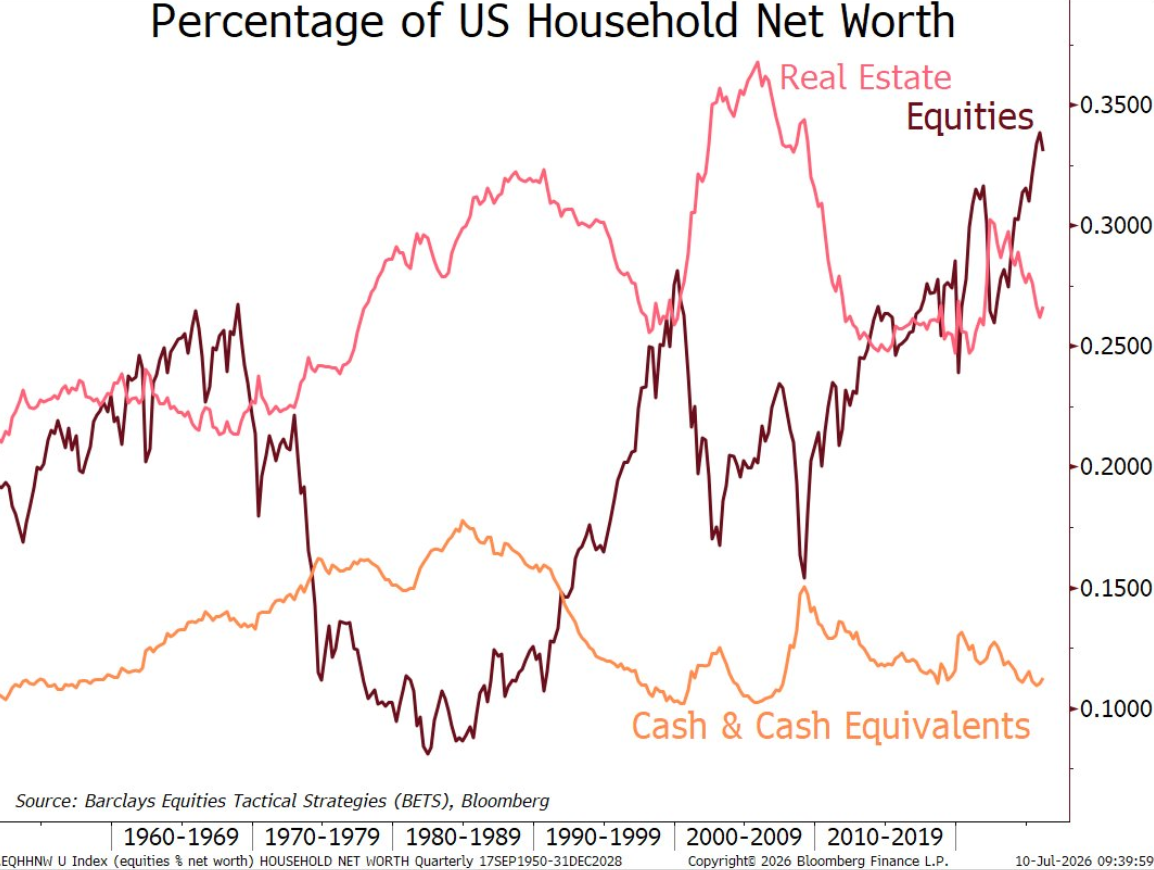

Joe Weisenthal shared an interesting chart of household allocations to various financial assets over time:

This chart might be something of a Rorschach test.

These allocations have been cyclical over time. Booms and busts. Leaders and laggards.

It’s quite possible that equities taking the lead by such a wide margin shows that they’re overvalued or possibly due for a pullback.

It’s also possible that this is a new normal of stock market dominance as an asset class.

I’m fascinated by changes to financial market structure over time, so much so that I devoted an entire chapter in Risk & Reward to a short history of household stock market ownership.

For much of the 20th century, the majority of U.S. households were underinvested in stocks. There were a variety reasons — a lack of disposable income in the pre-WWII days, high barriers to entry, high costs and a general lack of market knowledge.

It’s also true that pensions were more prevalent in the past. Not everyone had a pension in the past but defined benefit plans were a big part of retirement savings before defined contribution plans came along.

However, that doesn’t mean all of those pension plans were heavily invested in stocks. Pensions acted more like bonds for individuals but the plans themselves were relatively conservative investors in the past.

Peter Bernstein discussed this in an interview with PBS from the 1990s:

When I came into this in 1951 nobody of my generation was interested [in the stock market]. Everybody in the market was older…and they knew a great deal because they’d all survived this terrible experience (1929). And they were all terribly conservative in the way that money was to be managed. And there were laws, too. I mean, you couldn’t put a personal trust more than 35 percent in common stocks in New York. And in some states you couldn’t own any common stocks in any kind of a legal fiduciary. There’s some state that’s just now is changing. The state pension fund is mandated zero in equities.

The Great Depression created a generation of risk averse investors.

We don’t have that problem anymore.

First it was IRAs and 401ks. Then came online trading. Now we have zero dollar commissions, robo-advisors, targetdate funds, Robinhood and a whole host of platforms that will allow you to gamble away your life savings at the push of a button.

Everything is a financial market and the king of them all is the stock market. The United States makes up just 4% of the world’s population, 25% of global GDP but 65% of the world’s stock market capitalization.

The stock market is so important now that Bloomberg’s Eric Balchunas is asking if the Fed will buy stocks during the next financial crisis:

Eric makes the case that the stock market is our retirement fund. It’s the biggest stock market in the world (by far). There are more ways than ever to access stocks so the importance will only grow. Plus, Japan and China have already done this and investors assume the Fed has their back during a crisis.

Many will scoff at this idea. I don’t think it’s too far fetched depending on how bad the next crisis is.

Regardless of what happens in the next downturn, the stock market will remain more important than ever.

Retirees rely on stocks to hedge inflation. Pension plans are now heavily invested in stocks. More young people than ever have money in the markets. The automatic investing revolution means millions of people put money into the stock market on a regular basis regardless of what’s going on in the world.

The trillion dollar question is what does this mean going forward?

There are likely to be unintended consequences no one can foresee just yet but allow me to take a stab at it.

The markets are likely to force the hand of policymakers in the future. There will be more flash crash bear markets and corrections going forward.

This all started with the original TARP vote in 2008. The House rejected the $700 billion bailout fund so the stock market fell almost 9% the next day to force their hand.

The stock market falling 35% in a matter of weeks surely played a role in the trillions of dollars in government spending in such a short period of time during the early days of Covid.

The tariffs were walked back following the swift 19% drop in the stock market in a matter of days.

Energy prices spiking have played a role in how the Iran conflict has played out.

Investors know the stock market is more important than ever.

That probably means faster corrections and bear markets than we’ve seen historically.

But make no mistake — the stock market is in the driver’s seat now.

This is the new normal.

Further Reading:

Don’t Fight the Stock Market