No, not that regime change.

Swapping out Kevin Walsh for Jerome Powell will not matter much — to either inflation narrowly or the economy more broadly.

This is because the dominant theme in government policies – the one driving the overall economy – is less susceptible to FOMC action in this regime than in the last. The entire post-financial crisis era (aka the 2010s) was driven by monetary policy. The era during and after the pandemic was characterized primarily by fiscal policy.

This is why the Fed was unable to get inflation up to 2% in the 2010s; it’s also why the Fed has had such difficulty getting inflation down to 2% in the 2020s.

What made the GFC unique was the over-reliance on monetary policy. Following the credit-driven collapse of the financial crisis, the biggest risk to the economy was DE-Flation, that gravitational pull toward zero. Between ZIRP (2008 to 2015) and $3.6 trillion in quantitative easing (QE),1 Disinflation was the driver. PCE stayed under 2%, as soft job creation and wage gains kept consumer spending modest and inflation expectations anchored.

Congress abandoned its usual playbook and let the FOMC do all the heavy lifting. The post-GFC era was notable for a lack of fiscal stimulus – along with (not coincidentally) weak job and wage numbers.

QE and ZIRP primarily benefited capital, not labor; stock and bond holders did well; real estate owners saw a recovery, followed by price gains. Creditworthy individuals and healthy companies each refinanced their outstanding debt at low cost.

Credit was cheap, and Capital was practically free.

That changed during the pandemic era and beyond (2020–Present) as the opposite regime took hold. As Jerome Powell put it last August at Jackson Hole, “As it turned out, the idea of an intentional, moderate inflation overshoot had proved irrelevant.”

The foolish GFC fiscal austerity – including sequester and debt ceiling fights – was replaced with the largest peacetime fiscal expansion in U.S. history. This, combined with Powell’s “intentional overshoot,” helped to drive inflation up to 9%. Congress failed to engage on the fiscal side following the GFC; they wildly overcompensated for this error during the pandemic).2

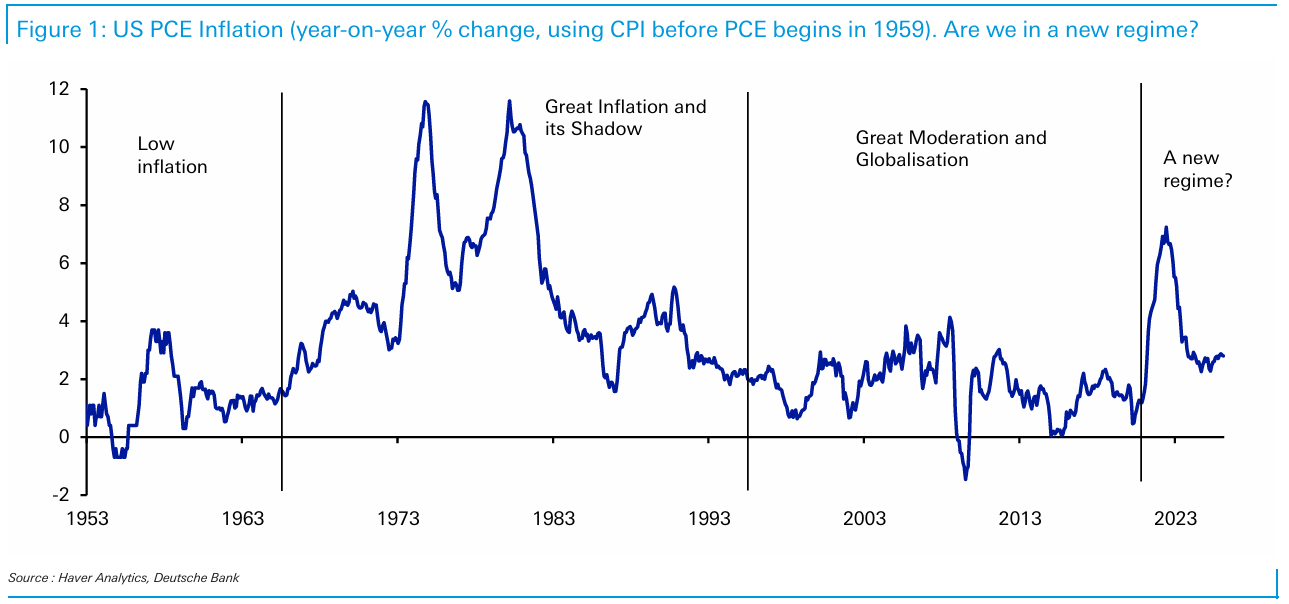

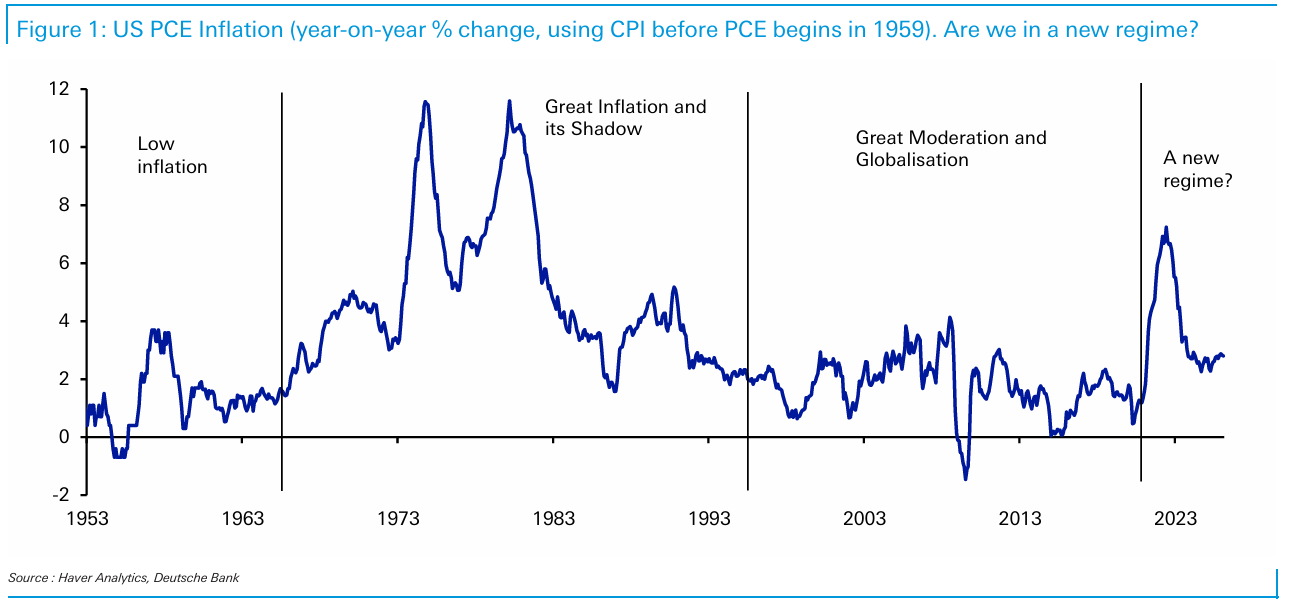

The chart above is from Deutsche Bank’s Jim Reid – he points out that the change from lower inflation was inevitable:

“Whilst many thought we were in a permanent period of lower inflation, the post-pandemic era has shattered many of those assumptions. We had already passed peak globalisation and the point of most supportive demographics by the mid to late 2010s, foreshadowing future inflationary pressures. But then the record peacetime stimulus of the Covid period, combined with significant supply chain disruptions, accelerated this trend. Then a war-related energy spike in 2022 further cemented inflation, and in 2026 we’re faced with another energy shock from the Iran conflict.”

Forget Warsh for Powell; swapping Fiscal for Monetary policy is the regime change that matters.

Previously:

2% Inflation Target is Silly (July 26, 2023)

The Fed is Finished* * (…Raising Rates) (November 1, 2023)

Inflation Comes Down Despite the Fed (January 12, 2023)

Why Is the Fed Always Late to the Party? (October 7, 2022)

Five Ways the Fed’s Deflation Playbook Could Be Improved (Businessweek, August 18, 2023)

Who Is to Blame for Inflation, 1-15 (June 28, 2022)

__________

1. To say nothing of Operation Twist, and the use of forward guidance as a policy tool…

2. Raise your hand if you think you know why!

__________

1. To say nothing of Operation Twist, and the use of forward guidance as a policy tool…

2. Raise your hand if you think you know why!