A reader asks:

I’m in my mid 30s and pursuing FIRE. If all goes well my wife and I should hit our target number by age 40. I’m not a big fan of bonds and rather just keep a larger cash position in a high-yield savings account equivalent to around two years of expenses and maintain a more aggressive mix of US and international ETFs. My question: does this make sense to do? Am I leaving money on the table by using only cash/savings and avoiding bonds or some other lower risk alternatives?

I’ve been getting a lot of questions recently about the desire to be financially independent and retire early. Many people really want to retire at a relatively young age. We can talk about the FIRE movement another time.

This is an asset allocation question. I enjoy asset allocation deep dives.

Let’s do this.

This person is asking about a barbell portfolio.

On one side of the barbell you have risk assets (stocks) and on the other side you have a risk-free asset (cash).1

Bonds are closer to cash than stocks on the risk spectrum, since both are technically fixed-income assets, though some consider them to sit in the middle of the bar in this analogy.

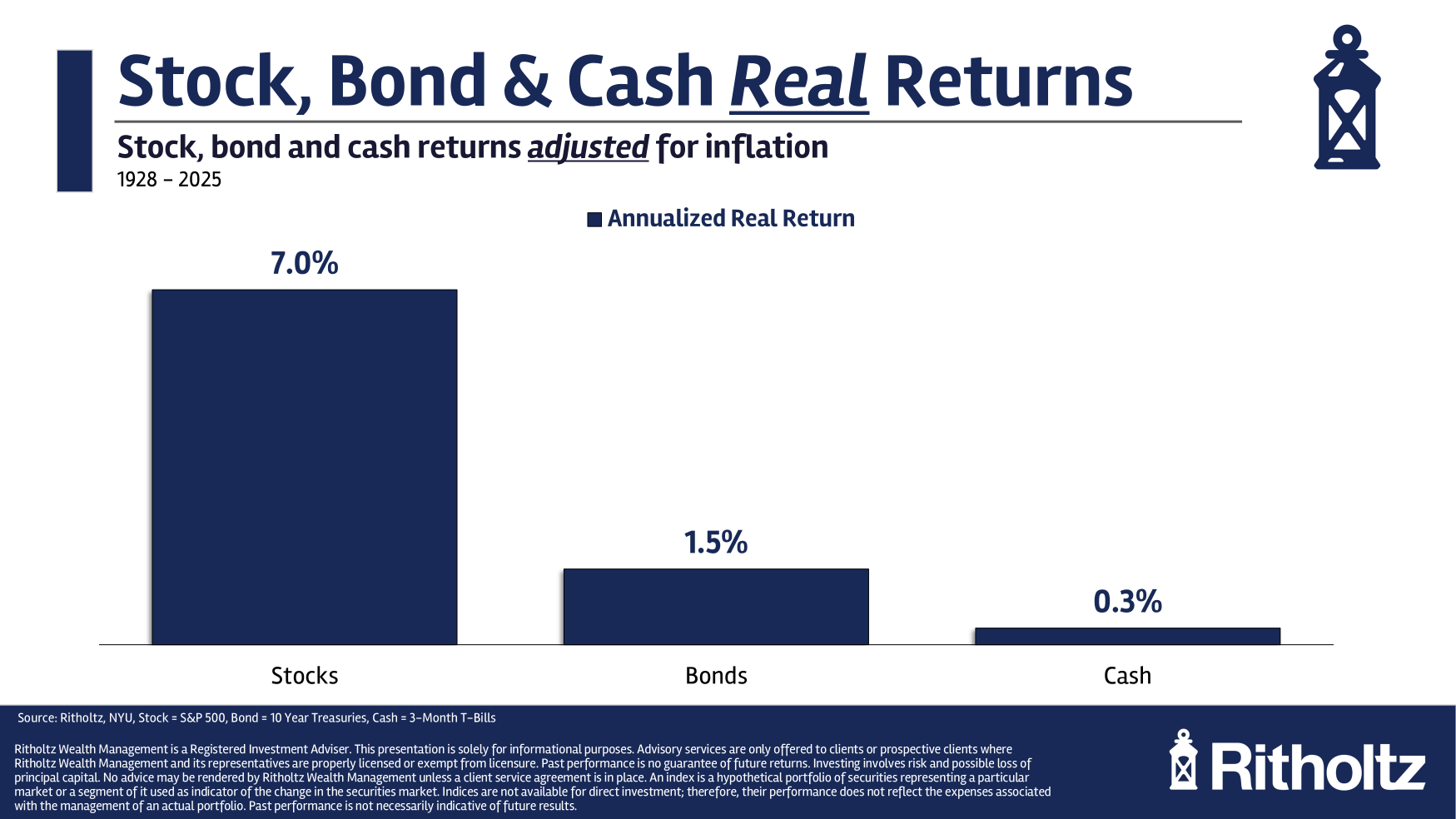

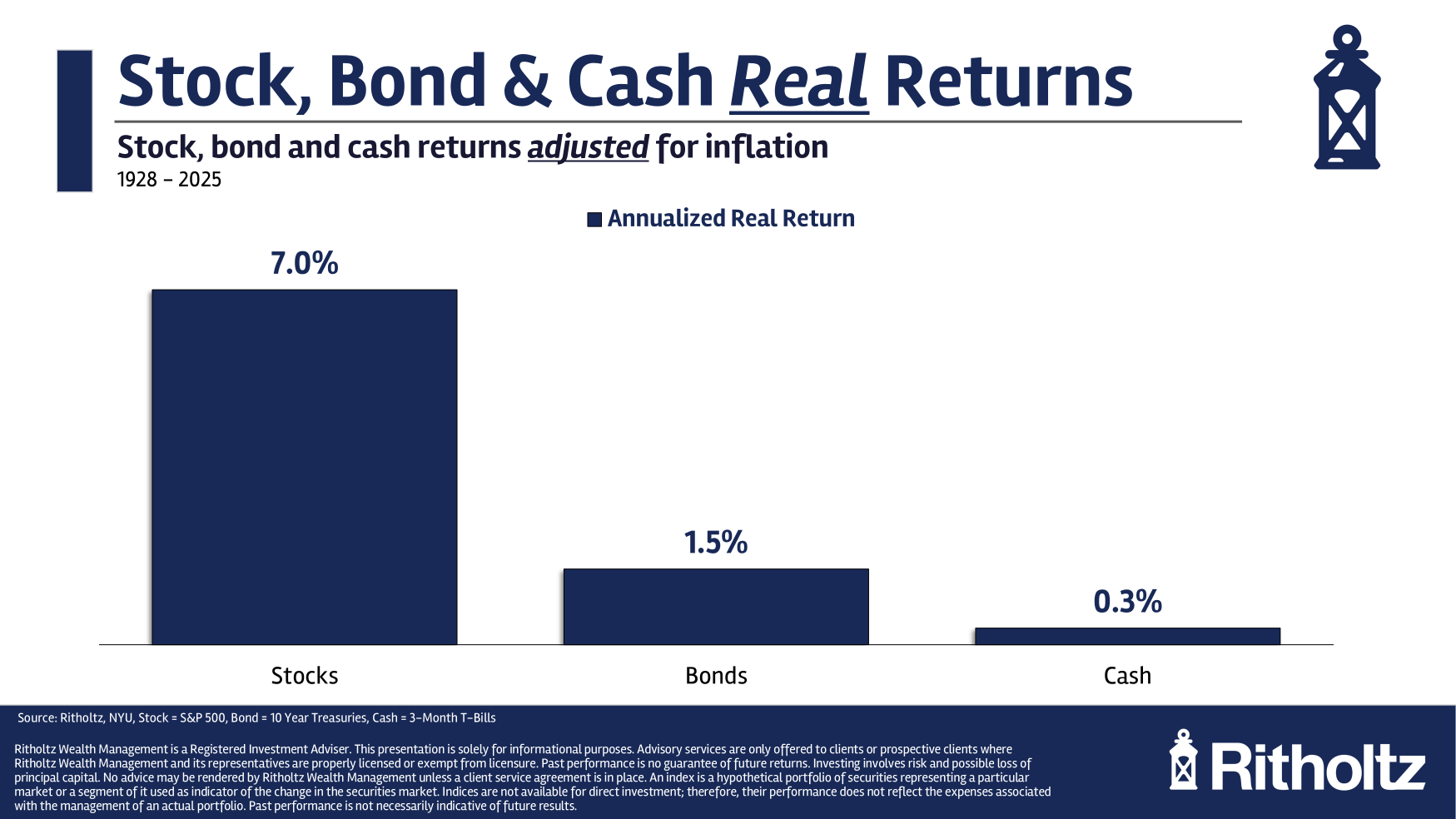

Here are the historical annual returns for each of these three main asset classes:

Cash returns have been relatively close to bond returns over the long haul.

Of course, the biggest risk for any fixed income investor is inflation. Here are the real returns adjusted for inflation:

The good news is that a cash position has kept up with inflation over time. The bad news is that you would not have earned much more than the rate of inflation.

There are a lot of investors who would rather not own bonds in their portfolio anymore. You don’t have to go searching for an answer too far on this one.

Just look at the returns in 2022:

- S&P 500 -18.0%

- 10 year Treasuries -17.8%

- 3-month T-bills +2.1%

Rapidly rising rates combined with rapidly rising inflation can be a nasty combination for government bonds. But short-term T-bills did just fine thank you very much. You don’t have to worry about interest rate risk when it comes to a cash-like position.

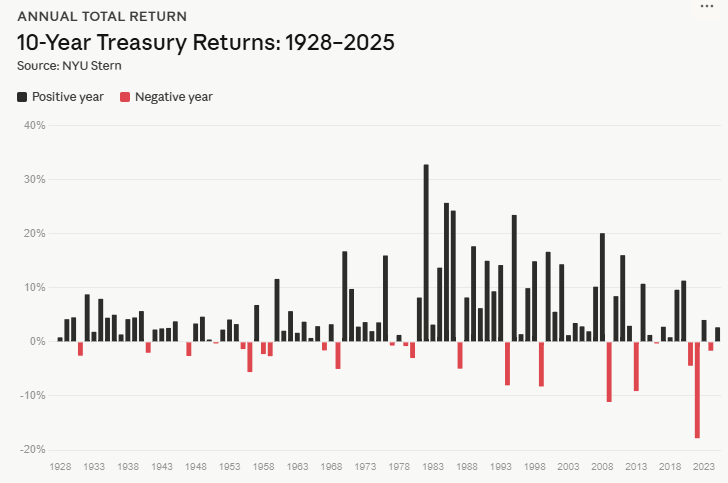

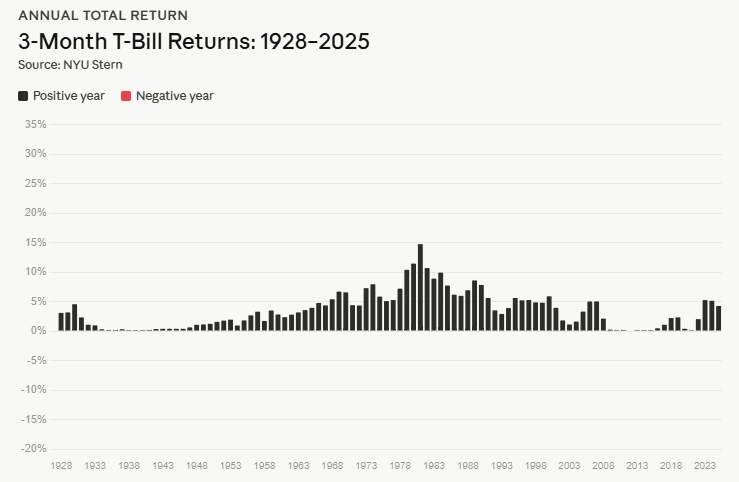

Let’s look at the differences in annual returns between bonds and cash to see why this is the case.

Bonds up first:

Now T-bills:

I used the same scale on these charts for a reason. Bond returns can be much higher than cash returns but there have been a decent number of down years for Treasuries. I count 19 down years for bonds which means the win rate is around 80%.

For cash there were no down years.

This is why many investors are now coming around to the idea of an allocation to cash in a barbell-like portfolio.

T-bills are one form of cash investment but this could also be a high yield savings account, money market or CDs.

So far we’ve been looking at the very long-run data here. It’s also helpful to think about risk in terms of shorter time frames. Certain environments are better for bonds, and others are better for cash.

This cycle has been much better for cash.

From 2022 to 2025 these are the annual returns for each:

This has been quite possibly the worst decade ever for bonds.

However, if you set aside some recency bias it wasn’t that long ago that cash was trash. The Fed kept interest rates on the floor for much of the post-GFC era. In fact, the average 3-month T-bill yield from 2008 to 2021 was just 0.55%.

Guess what the annual return was in that time? Around 0.5% per year. In that same time frame, the 10 year Treasury was up about 4% per year.

There have been other periods when the returns have diverged considerably in the past as well.

The combination of the Great Depression and World War II led to a prolonged period of financial repression with ultra low short-term interest rates from 1932 through 1954:

Cash underperformed bonds by a wide margin and lost money to inflation as well (which was 2.7% per year).

In the inflationary period from 1966 to 1981, cash was king:

Bonds got smoked from rising rates and sky-high inflation, while cash outperformed. Short-term rates adjust more quickly so you don’t have to worry about rising rates as much with a cash-like position.

I could keep going with these types of comparisons. The point is that the economy is cyclical, so the performance of fixed income assets will be cyclical too.

The big risk for bonds will be rapidly rising interest rates. The big risk for cash will be the Fed keeping short-term rates low for an extended period. The big risk for both bonds and cash will be high inflation.

Holding your spending reserves in cash makes sense from a liquidity perspective. You don’t have to worry about your nominal value going down.

But there are other risks to consider.

It really depends on how much you care about the yield, inflation protection and deflation protection.

I covered this question in more detail on an all new episode of Ask the Compound:

Bill Sweet joined us to discuss questions about de-risking equity risk in retirement, hitting your retirement number, taking care of your parents financially, talking yourself off the ledge of selling stocks and some advice for a teenage investor.

Further Reading:

The 4 Year Rule For Retirement Spending

1I’ve never been super comfortable with the term ‘risk-free’ because every investment involves risk in some form. It’s finance jargon. I need to get over it.